Alpha Hunter Portfolio Update (Jul 28 2022)

SEE ACT WIN's flagship strategy to consistently outperform the markets with lower risk

Summary

4.0% annualized outperformance over S&P500 ETF with 57% lower risk than the S&P500 ETF using a highly scalable, long-only, no-leverage, fully-invested, global large and mid-cap equity strategy. On track to create one of the best risk-adjusted investing records of all time.

Please see the introductory post on Alpha Hunter to understand it better.

Alpha Hunter Portfolio (Jul 28 2022)

Here are the portfolio characteristics as of Jul 27 2022:

Alpha Hunter Strategy Results

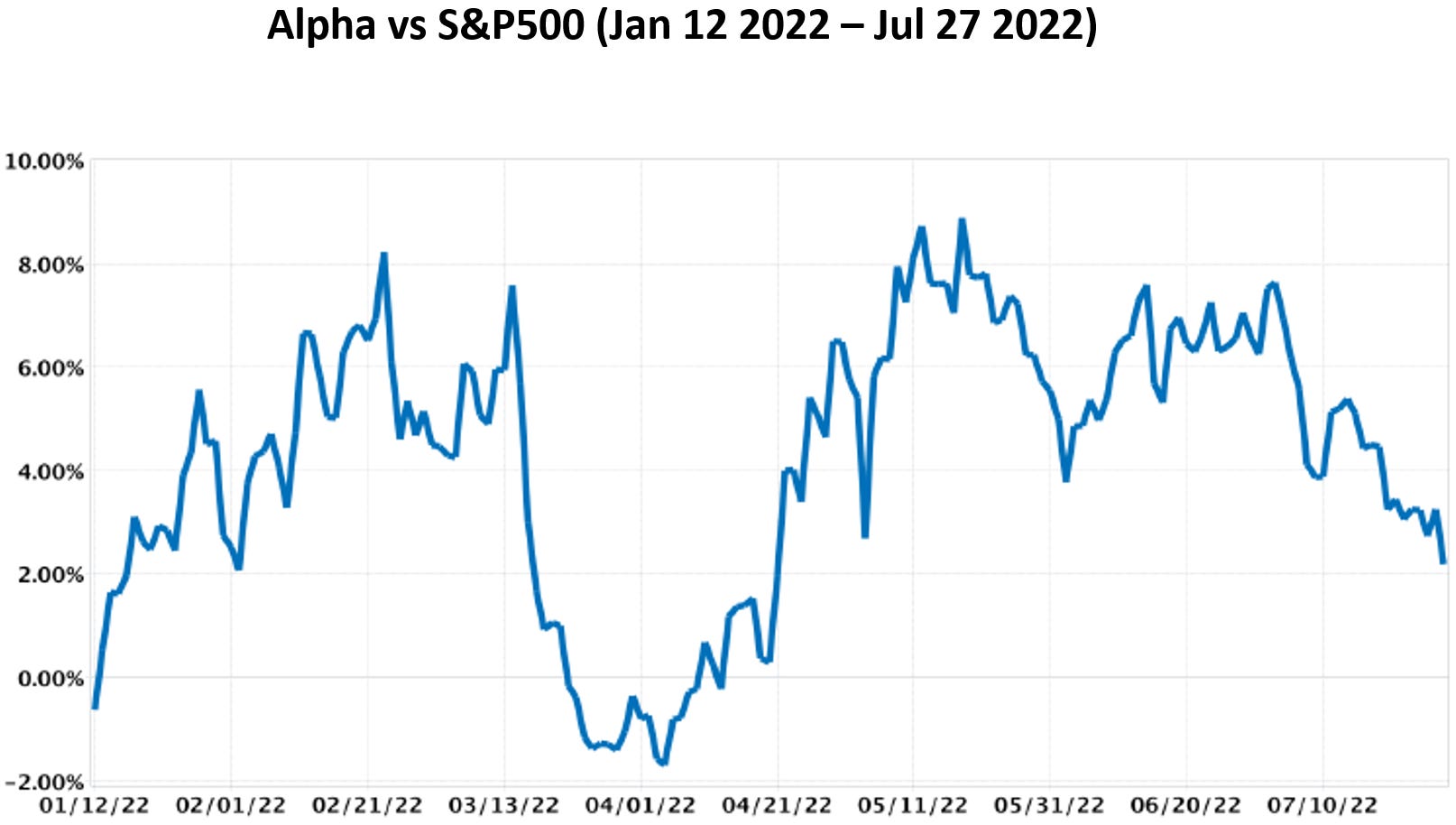

Here is a chart of the alpha generated vs S&P500 over time, net of all fees:

The steep fall in alpha during the middle of March 2022 and early May 2022 is not fully attributable to the Alpha Hunter stock selection process as these instances were due to our allocation decision mistakes wherein the portfolio was ~60% in cash and upto 100% in cash respectively when the market was rebounding sharply. The impact of this mistake was a ~5% and ~3.5% erosion in alpha, respectively. It was a risky deviation from the ‘Fully-invested almost all of the time’ characteristic of the strategy (see original Alpha Hunter strategy brief).

Alpha Hunter is currently going through some drawdown in alpha. But we remain confident in our positioning.

Since Jan 12 2022 till Jul 27 2022, Alpha Hunter has returned a time-weighted return of -11.76%, whilst the S&P500 has returned a time-weighted return of -13.90%, implying an alpha of +2.15%. This corresponds to an annualized alpha of 4.0%.

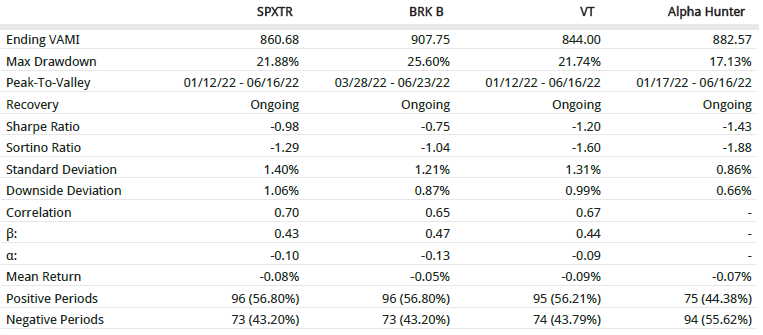

Here is a summary of key performance and risk statistics, net of all fees:

SPX500 Total Return Index, Berkshire Hathaway Class B stock, and Vanguard’s Total Stock Market Index are used as benchmark comparisons

Alpha Hunter outperforms other benchmarks; ~1.4% higher value-added monthly index (VAMI)

Alpha Hunter’s outperformance comes with a significantly lower risk:

Much lower standard and downside deviations; only 66% as volatile as the benchmarks

Much lower max drawdown; only 74% of the benchmarks’ max drawdowns

Low 0.40s beta; ~55% lower volatility than the market

Alpha Hunter’s Information Ratio (IR) vs the S&P500 Total Return Index is 0.13. Given that the strategy invests mostly in large-cap global stocks, this places the performance of Alpha Hunter closer to the 25%ile of funds than the median:

Source: Informa Investment Solutions

Disclosure

Solutions must fit the circumstances and conditions present in the goal or problem. Without knowing these circumstances and conditions, it is impossible to prescribe a specific solution! This is a general principle.

We do not know our readers’ circumstances or conditions present in their financial status and goals. Hence, we cannot prescribe or recommend any specific solution. Therefore, please view what we write about simply as our humble opinion, which you are free to consider or not consider in whatever way you wish for any way you approach decision-making.