Beat the Market with Alpha Hunter

SEE ACT WIN's flagship strategy to consistently outperform the markets with lower risk

Summary

Consistent 14.5% annualized outperformance over S&P500 ETF with 58% lower risk than the S&P500 ETF using a highly scalable, long-only, no-leverage, fully-invested, global large-cap equity strategy. On-track to create one of the best risk-adjusted investing records of all time.

What is Alpha?

Alpha in the financial markets means outperformance over something (for example a market index)

An investment strategy is only worth something if it can generate alpha at an acceptable level of risk (ideally lower risk)

In the context of Alpha Hunter, alpha refers to outperformance over the S&P500 index

How I SEE Reality in the Markets

The market moves according to the incremental buy or sell actions of its participants

Incremental changes in the market sentiment are reliable, leading signs of the incremental buy or sell actions

The fundamentalists have an incomplete framework, especially if investment is from a minority investors’ perspective; market sentiment is the primary source of truth in the markets

The market reflects the fundamental view of stocks only if its participants act according to that view. But this does not always happen. For example, in broad stock market bubbles, the market has defied the fundamentalists' view of 'intrinsic value' for over a decade! In other words, the fundamentalists would have been wrong for almost 10 years! See my Twitter thread on Market Bubbles for more context.

Having a sentiment-focused approach to the markets benefits from a faster feedback loop to be in tune or slightly ahead of the market action more frequently. This helps in consistent alpha generation (which can be measured via high information ratios; see the ‘Alpha Hunter Strategy Results’ section below)

What is Alpha Hunter?

Alpha Hunter is an investment strategy that makes consistent, low-risk alpha by investing in the global financial markets

Alpha Hunter is a strategy that continuously adapts to the market using unique, proprietary methods I have created to accurately read the shifts in market sentiment. Alpha Hunter is an outcome of both systematic and discretionary inputs with strong empirical backing.

The continuously adaptive nature of the strategy makes it structurally immune to most factor and ‘investment philosophy’ biases (the market can behave oppositely to how your philosophy expects it to behave for far longer than you can tolerate)

Alpha Hunter is proving itself to be a superior alternative to index-investing with lower risk (see proof below in the "Alpha Hunter Strategy Results Section")

Characteristics of Alpha Hunter

Long-only

Aligned with how the markets are structurally bullish most of the time

Opportunistic shorts or cash exposures can add alpha, but it also increases the risks in the strategy. Currently, this is not a main part of the Alpha Hunter strategy, but may be implemented under compelling circumstances.

Fully invested almost all of the time

Markets are structurally bullish most of the time

Market corrections tend to be sharp and violent

Missing the few sharp rebounds in market corrections can seriously erode returns as this table shows:

Source: Bank of America, S&P500 returns

But during times of genuine market-wide bubbles, this fully-invested policy is subject to change. Read this thread on how I view Market Bubbles to see why:

No leverage

To avoid flash-crash/whipsaws risk that can destroy one’s capital. Currently, I have no reliable ability to anticipate the extent of these drawdown risks

Plain vanilla stocks and ETFs; no options, futures and other derivatives

Playing derivative instruments requires more assumptions about how markets behave

More assumptions increase the chances of being wrong

I have high confidence in generating significant alpha without the use of riskier derivative instruments

Global equity investable universe in the most liquid (mostly large-cap) instruments:

Amsterdam (AEX 25)

France (CAC 40)

Nordic (OMX Copenhagen 25)

Germany (DAX 40)

Estonia (OMX Tallin)

Belgium (EURONEXT BRUSSELS 20)

United Kingdom (FTSE 100)

Finland (OMX Helsinki 25)

Iceland (OMX Iceland 10)

Israel (Tel-Aviv 125)

Lithuania (OMX Vilnius)

Mexico (BMV 35)

United States (S&P 500)

Singapore (Strait-Times 30)

Sweden (OMX Stockholm 30)

Europe (EURO STOXX 50)

Japan (Nikkei 225)

Hong Kong (Hang Seng)

Canada (TSX 250)

Australia (ASX 200)

Allocation ETFs

Alternative ETFs

Commodity ETFs

International Equity ETFs

Other US Equity ETFs

VOO ETF from Vanguard is the proxy for the S&P500 benchmark

Global access allows me to go wherever the opportunity is present

India, China and other emerging markets are not included due to accessibility constraints for the typical retail investor

The total investable universe currently consists of more than 2,000 stocks and ETFs

Mix of active alpha picks and S&P500 ETF exposure

Active alpha picks are used to generate alpha

All alpha picks are equally weighted at initiation. There is further scope for optimization of this parameter.

The selection criteria for Alpha Hunter’s active alpha picks is very strict. On average, less than ~1% of the investable universe makes it into the Alpha Hunter’s active alpha portion of the portfolio

A S&P500 ETF is our default passive benchmark as it is a broad-based ETF that is widely accessible and affects a large part of global stock markets. It is deemed to be a good proxy for the next-best-alternative for most investors.

When the US catches a cold, the whole world sneezes

Proceeds from exits of active alpha picks are deployed into the S&P500 ETF until new active alpha picks are generated. This is done to preserve the realized alpha.

Active Strategy

To stay closely in-tune with the best alpha opportunities in the market, turnover of the portfolio will be high (annualized turnover of almost 49x implies the entire portfolio refreshes almost 49x in a typical year)

High turnover is not necessarily bad; it often happens because the alpha is captured sooner rather than later, which makes for efficient use of capital

>12 month holds are extremely unlikely, which implies no long term capital gains tax discount. But this is expected to be more than offset by significantly higher alpha, net of all fees

My Confidence in Alpha Hunter

I understand that it is difficult for most investment managers to generate alpha over decades. I understand how dangerous it is to be confident of oneself in the financial markets. I understand the many pitfalls and risks in various high-return investment strategies. Yet, I truly believe Alpha Hunter is different and superior.

With Alpha Hunter, I am on-track and expect to continue generating alpha that will eventually earn a place in the record books, along with the greatest investors of all time:

Yes; that is how confident I am in Alpha Hunter

Excluding my real estate investments, ~80% of my remaining personal net worth is allocated to the Alpha Hunter strategy.

Alpha Hunter Strategy Results

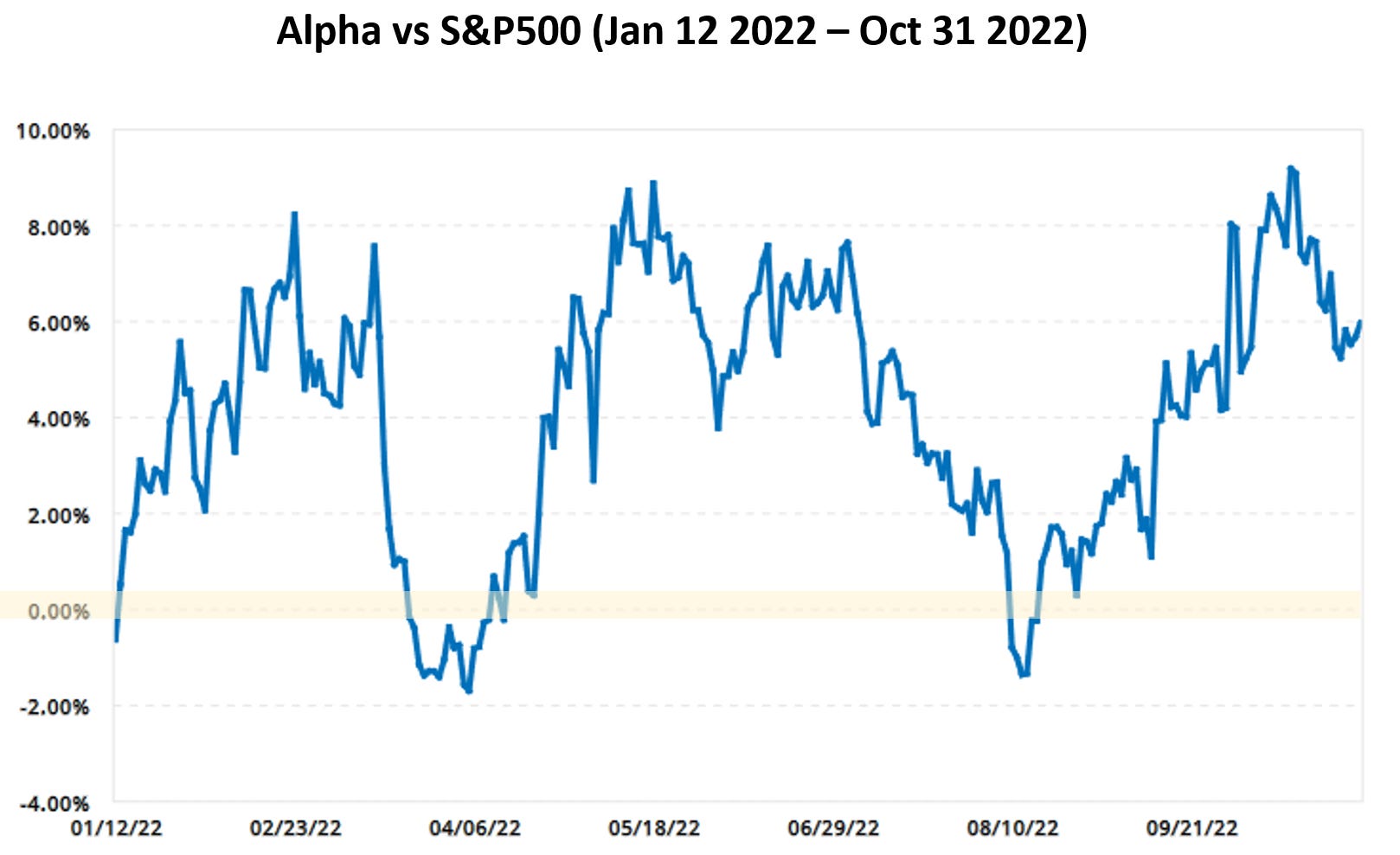

Here is a chart of the alpha generated vs S&P500 over time, net of all fees:

The steep fall in alpha during the middle of March 2022 is not fully attributable to the Alpha Hunter strategy. This was due to an allocation mistake wherein the portfolio was ~60% in cash for too long when the market rebounded sharply. The impact of this mistake was a ~5% erosion in alpha. It was a risky deviation from the ‘Fully-invested almost all of the time’ characteristic of the strategy. I do not expect such mistakes to occur again.

Since Jan 12 2022 till Jun 24 2022, Alpha Hunter has returned -10.11%, whilst the S&P500 has returned -16.42%, implying an alpha of +6.31%. This corresponds to an annualized alpha of 14.5%.

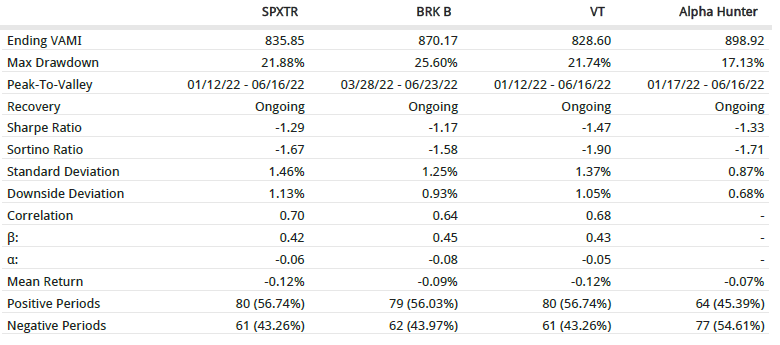

Here is a summary of key performance and risk statistics, net of all fees:

SPX500 Total Return Index, Berkshire Hathaway Class B stock and Vanguard’s Total Stock Market Index are used as benchmark comparisons

Alpha Hunter outperforms other benchmarks; ~6.5% higher value added monthly index (VAMI)

Alpha Hunter’s outperformance comes with significantly lower risk:

Much lower standard and downside deviations; only 64% as volatile as the benchmarks

Much lower max drawdown; only 74% of the benchmark max drawdowns

Low 0.40s beta; ~57% lower volatility than the market

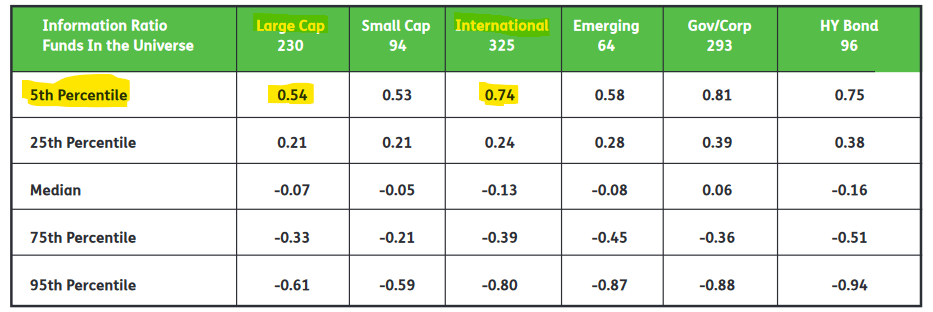

Alpha Hunter’s Information Ratio (IR) vs the S&P500 Total Return Index is 0.67. Given that the strategy invests in large-cap global stocks, this places the performance of Alpha Hunter within the top 5%ile of funds:

Source: Informa Investment Solutions

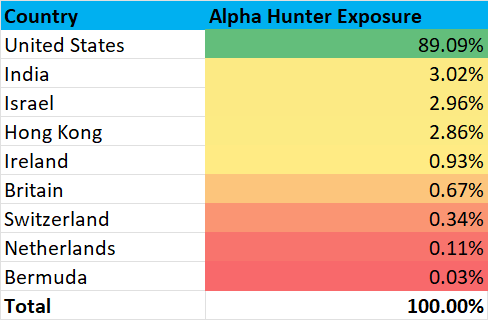

Alpha Hunter Portfolio (Jun 24 2022)

Risk Control on Alpha Hunter

Alpha Hunter is a very risk-responsible strategy that avoids virtually all 7 Deadly Sins of Portfolio Management:

Excessive Leverage

Alpha Hunter uses 0 leverage

Excessive Concentration

Alpha Hunter caps individual active alpha selection’s exposure at 3.0% of the portfolio

Excessive Correlation

Alpha Hunter tends to be a well-diversified portfolio

Illiquidity

Alpha Hunter invests only in the largest, most liquid stocks in global markets

Capital Flight

Alpha Hunter is not a fund currently. There is 0 redemption or forced selling risk

High Flyers

Alpha Hunter is a low-beta portfolio with a more defensive slant; it is relatively immune to chasing market euphorias and thus avoids getting caught in bubbles

Fraud

Alpha Hunter invests in the largest stocks in global equities with ample coverage by professional investors and sell-side research. This reduces the chances of getting caught in frauds.

Scalability of Alpha Hunter

In its current form, it would be difficult to scale Alpha Hunter to levels with hundreds of billions of dollars under management. However, as the strategy focuses exclusively on the most liquid, large-cap stocks in a particular market, based on preliminary liquidity constraint checks, the strategy is deemed to be scalable for at least >USD1bn in assets under management (AUM).

What if Alpha Hunter Underperforms?

Every edge in the markets is prone to erosion.

The critical question is how soon can deterioration of a strategy’s edge be detected to take corrective action or halt the execution of the strategy?

Some long-term investing strategies have feedback loops lasting decades, which leads to a very late and highly impractical means of detecting and fixing a broken strategy.

Alpha Hunter has a high-frequency feedback loop, and it dynamically adjusts to the changing sentiments of the market. Every position is monitored daily, and active alpha selections that are not working as per expectations are cut and replaced during a typical turnover cycle (weekly to monthly).

In the case of 6 months of negative alpha results, I would initiate a full strategy review to diagnose and fix broken aspects of the strategy before deploying additional capital on active alpha selection picks. During this time, the portfolio would largely track the benchmark S&P500 ETF to preserve alpha.

Replicating the Alpha Hunter Portfolio

Access to Global Markets is necessary to replicate the Alpha Hunter portfolio.

I use Interactive Brokers. It is the lowest-cost brokerage with the widest global market access, used often by professional and institutional investors. In contrast, many retail brokerages rip you off in more ways than is apparent. Don’t get ripped off. If you would like a mutually beneficial referral code, email rajarishtocrat@outlook.com and I may give you one.

Access to US markets is very important for the successful execution of Alpha Hunter; if one does not have access to other global markets, one can replace that foreign stock with a S&P500 ETF (such as VOO by Vanguard).

Daily LIVE portfolio status and ALL buy/sell updates will be shared via Twitter and Substack for FREE

Alpha Hunter is a Blue Ocean Strategy

In my opinion, considering how Alpha Hunter is fully built using in-house methods to read incremental changes in market sentiment, this is a unique strategy for playing the global equity markets. Currently, on aggregate, there is minuscule capital allocated to this strategy relative to the capacity of Alpha Hunter (at least USD1bn, if not more). In simpler words, liquidity constraints are a long way away for Alpha Hunter.

Hence, Alpha Hunter is a blue-ocean approach to playing the markets; there is currently enough capacity for many market participants to benefit from the successful results of Alpha Hunter.

Therefore, if you find Alpha Hunter to be of value to you in any way, please do share and spread the word. This really helps me.

Disclosure

Solutions must fit the circumstances and conditions present in the goal or problem. Without knowing these circumstances and conditions, it is impossible to prescribe a specific solution! This is a general principle.

I do not know our readers’ circumstances or conditions present in their financial status and goals. Hence, I cannot prescribe or recommend any specific solution. Therefore, please view what I write about as research that I am sharing with you, for you to consider in however you approach decision-making.