Deterra Royalties (DRR)

An Australian Mining Royalty Company that is not worth the price

Summary

Highly optimistic iron ore prices and extensions of mine resource life would need to be assumed to justify a meaningful upside for Deterra Royalties. The stock is judged to be currently overvalued by 17%.

Industry Analysis

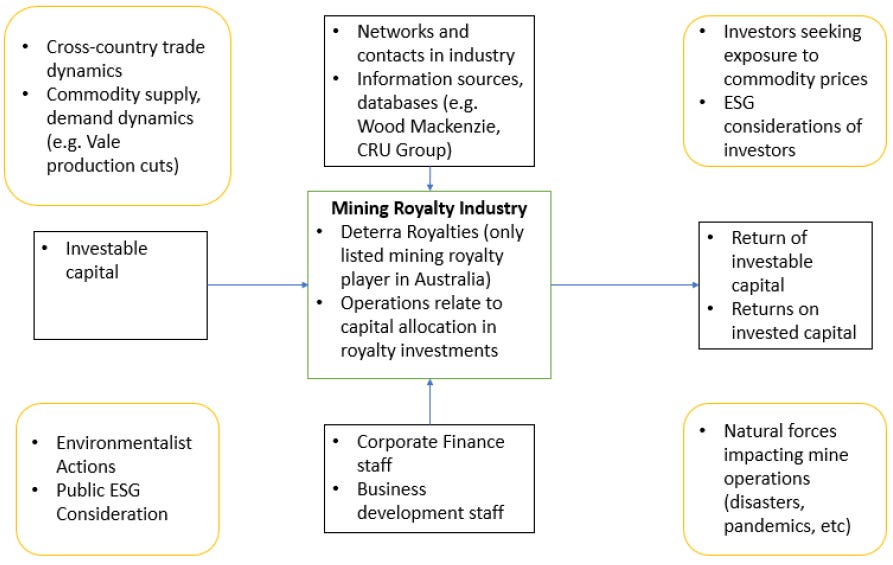

Value Chain

The mining royalty industry model is unique but simple. The industry structure is very similar to that of the fund management industry as the key input is investable capital.

The key operations for a mining royalty player involves making capital allocation (investing) decisions to buy royalty assets to generate an output in the form of returns on investable capital. To conduct these operations, knowledge is a key resource, acquired from industry contacts, experience and industry specific information databases such as Wood Mackenzie and CRU Group. The industry is very asset-light with very minimal labour requirements as well. For example, Deterra has only 6 employees! Besides the CEO, CFO and Investor Relations Head, they have a Senior Analyst, Business Development Manager and an Executive Assistant.

Cross-country trade dynamics, supply-demand dynamics of underlying royalty commodities, natural forces and ESG considerations of the public and investors all have an influence on operations in this industry’s value chain.

Size, Growth, Share

The Australian mining industry is worth AUD 315bn. According to industry experts, it is expected to grow annually at 0.1% over the next 5 years, driven by low output volumes growth and decline in export volumes. The industry is concentrated among 4 large, reputable players (BHP, Rio Tinto, Fortescue Metals and Glencore), which collectively have 40% market share. Over the past 5 years, the concentration has increased even more with all players gaining share except Glencore.

The Australian iron ore mining industry is worth AUD 129bn. China is a key demand driver in the industry, with almost 80% of industry revenue coming from Chinese steel manufacturers in 2021. The Australian iron ore mining industry is expected to shrink by 5.8% annually over the next 5 years, driven by increased global iron ore supply, flat output volumes and China’s goals to reduce dependence on Australian iron ore. BHP has 25% share in this industry segment, with the largest player Rio Tinto having 34% share.

For the royalty mining players, the increase in industry consolidation towards more reputable players yields an environment where there is higher supply of quality royalty mine assets for investments.

Success Factors

Disciplined capital allocation

Purchase of royalty mining assets at ideally a discounted value to generate excess returns for investors is critical for the success of the industry. To accomplish this, a team of industry experts with strong capital allocation skills is necessary.

Diversified portfolio

A royalty mining portfolio that is smartly diversified across different types of mining commodities (iron, mineral sands, coal, battery metals, precious metals, etc) in a way that reduces the overall correlations of the portfolio will de-risk the business profile.

Access to capital

Access to equity and debt financing for royalty mining assets is important to grow a royalty miner’s business portfolio.

Business Analysis

History

Deterra Royalties was formed from a demerger of Iluka Resources on 2nd Nov 2020. The rationale for the demerger was to split Iluka into 2 separate, economically different business segments; the mineral sands mining business that stays with Iluka and the royalty mining business that is hived off into Deterra Royalties. This demerger allows investors to isolate commodity price exposure via a play on Deterra Royalties without being affected by idiosyncratic explorational and operational risks that would come with a company such as Iluka Resources.

Business Profile

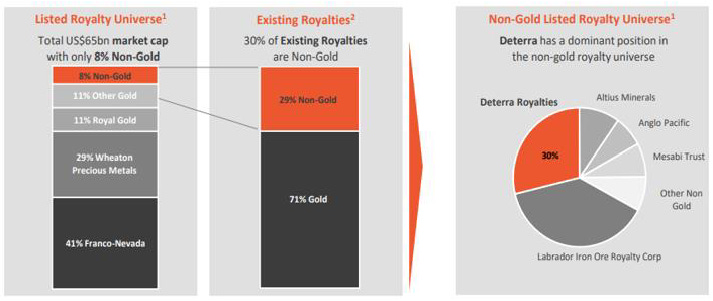

Deterra is the global market leader among non-gold mining royalty companies with 30% share. In Australia, it is the only listed mining royalty player:

Deterra has 6 royalty assets with exposure to iron ore and mineral sands such as titanium and zircon:

However, its business is highly concentrated with Mining Area C (MAC) contributing to 99.45% of total royalty revenues.

Mining Area C (MAC)

MAC is an iron ore (high 62%+ grade) mining facility operated by BHP. It is split into 2 major areas; a North Flank and a South Flank:

The North Flank has annual wet (iron with moisture) production of 65 million tonnes and annual dry (iron without moisture) production of 59 million tonnes. Only the North Flank has been in production since 2003. The South Flank came online in May 2021. The South Flank is expected to ramp up annual wet production to 80 million tonnes over the next 4 years, leading to a combined annual run-rate of wet production of 145 million tonnes. According to management, this corresponds to a combined annual run-rate of dry production of 139 million tonnes, implying a 93% yield.

The mine life of the North and South Flank is 30 years till 2050, but according to BHP, potential future development of Tandanya and Mudlark can extend the life another 23 years to 2073.

Under the royalty agreement, Deterra is entitled to 1.232% of AUD denominated quarterly freight-inclusive iron price-based revenue. There is also a capacity payment, whereby for every 1 million ton increase of dry iron ore annual production above historical maximum annual production, Deterra Royalties is entitled to a payment of AUD 1 million in that year.

Other Mines

The other 5 mine royalty assets are much smaller, contributing only 0.55% of total revenues. They are all either in decommissioned phase, with only stockpile sales occurring currently, not having any operations or in the process of getting approvals before starting operations.

Competitive Edge

MAC iron mines are positioned well in the cost curve within the 2nd quartile. Typically, global commodity prices trade at the 90th percentiles of the commodity’s cost curves. This means BHP’s MAC operations are comfortably within the profitable operations zone. This is advantageous for Deterra since BHP is highly unlikely to voluntarily close, halt or reduce production output from its profitable ventures in the MAC region.

Growth Strategy

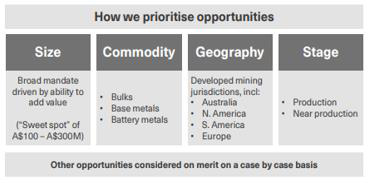

Deterra’s management plan to target global mining royalty assets of size AUD 100 million – AUD 300 million across non-precious metals to grow the royalty portfolio via acquisition. They intend to do future capital allocation on only production-active or near-production-active assets instead of riskier exploratory stage assets:

Management

It is critical to assess the management team’s capital allocation capabilities since acquisition of new royalty assets at attractive valuations is a key success driver for the business.

Julian Andrews has more than 20 years experience in project assessment, capital raising and capital allocation in the mining, energy and chemicals industries. Before becoming CEO of Deterra in October 2020, he was the Head of Strategy, Planning and Business Development at Iluka Resources for 3 years. Iluka Resources (ILU) underperformed the ASX 200 Resources sector (XJR) by 10.8% during his tenure at the company from September 2017 to October 2020.

Brendan Ryan has more than 26 years experience in the global mining sector. Before becoming CFO of Deterra in September 2020, he was the Chief Business Development and the Chief Financial at Boart Longyear, a global mineral explorations company. Boart Longyear (BLY) underperformed the ASX 200 Resources sector (XJR) by 99.1% during his tenure at the company from September 2016 to September 2020.

Overall, the management team is experienced in their sector and have held leadership roles in capital allocation functions before. However, the underperformance of their previous companies when they were tenured there is a potentially concerning sign. Based on this, there is no clear evidence to support that the CEO and CFO of Deterra Royalties are great capital allocators.

Key Business Driver

Besides production expansion via South Flank operations, the main driver of the current business portfolio is:

62% grade iron ore prices inclusive of freight cost

This affects the sales realization of the mined iron ore of grade 62%+ at MAC. The freight route applicable for dry (material without moisture) freight between Western Australia and China is C10_14 in the Baltic exchange. The following shows the chart of iron ore cost less freight cost in AUD currency:

In my model, I have assumed average FY22 freight-inclusive iron ore prices to be AUD 90. Thereafter, I have assumed a consistent 3% growth in iron ore realization prices (including freight cost) annually, in-line with inflation expectations.

Valuation

I have assumed the mining royalties continue till 2050, when the MAC mine life nears its end at current operational presence and estimated production rates. After 2050, I have assumed there is no free cash flow in the business. I believe assuming otherwise may be giving management too much benefit of the doubt about their value creation capabilities, given the track record of share price underperformance at their previous companies when they held leadership positions in capital allocation functions.

At an opportunity cost of capital of 6.8%, I get an equity value per share of AUD 3.29, which leads to a net downside of 17% from the current share price as at 22nd Oct 2021 of AUD 3.97.

Here is the valuation summary:

Here are the valuation sensitivities with the FY22 iron ore price, inclusive of freight cost assumption:

Here are the valuation sensitivities with the growth in the iron ore price, inclusive of freight cost after FY22:

Flows and Sentiment Analysis

The above shows a chart of DRR against the ASX 200 index (XJO). By analysing the chart of this spread of DRR vs XJO rather than DRR alone, it is possible to ascertain whether DRR would be a relatively better investment than the XJO index. Such a method of analysis helps in identifying market outperformance (alpha) opportunities with greater consistency.

Trend

DRR/XJO is in a downtrend as it is making lower highs and lower lows. This suggests that DRR is underperforming the ASX 200 index.

Key Levels

Price is close to a daily resistance level. DRR/XJO may resume the downtrend once it hits the purple line annotated in the chart.

Momentum

The movement of the buyers in the DRR/XJO chart is slow and weak, suggesting that there is no trend reversal underway. Hence, I expect DRR/XJO to continue being in a downtrend, thus leading to continued underperformance of DRR relative to the ASX 200 index.

Playing the Opportunity

I suggest a SELL on Deterra Royalties as both fundamental and sentiment analysis points towards a clear overvaluation of the stock, leading to a downside of 17% and fair value of AUD 3.29 per share. Key risks to this view include higher than expected iron ore price including freight, better than expected capital allocation by management, and extension of mine life beyond 2050.

Best,

Raj Arishtocrat